There was a time — not very long ago — when people inside shipping used to joke that nobody notices the industry unless something goes wrong.

Then came 2020.

Since then, I do not think there has been a single boardroom, commodity trader, retailer, exporter or government that has ignored shipping again.

And if someone wants to understand what really happened to global trade after the pandemic, they do not need to read ten economic reports. They only need to study the financial statements of A.P. Moller - Maersk from 2020 to 2025.

Because hidden inside those numbers is the entire emotional cycle of modern supply chains:

panic, shortage, greed, power, correction and finally exhaustion.

The numbers tell the story — but not the full truth

Year | Revenue | Profit of the year |

2020 | 39.7 bn | 2.9 bn |

2021 | 61.8 bn | 18.0 bn |

2022 | 81.5 bn | 29.3 bn |

2023 | 51.1 bn | 3.9 bn |

2024 | 55.5 bn | 6.2 bn |

2025 | 54.0 bn | 2.9 bn |

At first glance, it looks like a classic boom-and-bust cycle.

But after spending years watching ports, freight markets and exporters react to every disruption, I think something much bigger happened here.

The pandemic did not create a shipping boom.

It exposed how fragile globalization already was.

Before COVID, shipping had already become too cheap

People forget this part now.

Before 2020, container shipping was brutally competitive. Rates were weak for years. Carriers chased volumes more than margins. Bigger vessels kept entering the market, and everyone believed scale alone would solve profitability problems.

Shipping had become almost invisible to consumers because logistics costs were too efficient.

Then the system snapped.

2020 was not profitable because trade was strong

It was profitable because the world lost control of logistics.

I still remember those months when containers started piling up in the wrong places. Exporters could not find equipment. Ports were operating with labour restrictions. Trucking networks slowed down. Warehouses overflowed.

At first, many carriers expected losses.

Instead, something unusual happened:

cargo demand returned faster than transport capacity.

That imbalance changed the psychology of the industry overnight.

For decades, shipping lines had chased cargo.

Suddenly, cargo owners were chasing ships.

That was the beginning of the most profitable period container shipping has ever seen.

2021 was the year carriers realized they had power

You can see it clearly in Maersk’s numbers.

Profit jumped from USD 2.9 billion to USD 18 billion in one year.

That kind of increase does not happen because management suddenly became smarter.

It happens when the market breaks.

The shipping industry entered territory nobody had imagined before.

Freight rates became disconnected from historical logic.

Containers that used to move for USD 2,000 suddenly moved for USD 15,000 or more. Importers accepted almost any rate because empty shelves were becoming more dangerous than expensive freight.

And this is the important part many people outside logistics misunderstood:

The crisis was not just about ships.

It was about time.

Once schedules collapsed, the entire global supply chain became inefficient. One delayed vessel created another delayed warehouse, which created another delayed truck, which created another production delay.

Shipping was no longer transport.

It became the heartbeat of the world economy.

2022 was probably the peak of globalization itself

That may sound dramatic, but look at the scale.

Maersk earned almost USD 30 billion in annual profit.

A shipping line.

Not a tech company.

Not an oil producer.

A container carrier.

For people working around trade during those years, the atmosphere was surreal.

Freight forwarders could barely secure space.

Importers booked cargo weeks in advance.

Retailers over-ordered inventory because nobody trusted supply chains anymore.

Fear became part of procurement strategy.

And fear is extremely profitable for logistics companies.

The industry had pricing power that may never return again in the same form.

But beneath the surface, another problem was quietly building.

Everybody started ordering ships.

The shipping industry always repeats the same mistake

Shipping companies are famous for this cycle.

When profits rise, they believe demand will stay strong forever.

So they order more vessels.

Then those vessels arrive just when the market cools down.

That is exactly what happened after 2022.

The industry ordered capacity as if pandemic conditions would continue for years.

But by 2023, reality had changed.

Consumers slowed spending.

Inflation hit demand.

Warehouses became overstocked.

Port congestion eased.

And suddenly the market remembered something it had temporarily forgotten:

Container shipping is still a commodity business.

2023 felt like the hangover after a long party

The collapse was brutal.

Maersk profit fell from USD 29 billion to below USD 4 billion.

What fascinated me most during that period was how quickly the narrative changed.

Only months earlier, people were calling shipping lines unstoppable.

Then suddenly analysts started speaking about overcapacity again.

But if you looked carefully, Maersk itself was already changing.

The company understood something many traditional carriers still struggle with:

Ocean freight alone is too unstable.

That is why Maersk kept investing in:

logistics,

terminals,

warehousing,

inland transport,

e-commerce fulfilment.

It was trying to escape the old shipping cycle before the cycle returned completely.

Then the Red Sea crisis changed everything again

By 2024, another strange thing happened.

Geopolitics temporarily saved shipping profits.

The Red Sea disruption forced carriers to avoid normal Suez routes and sail around Africa instead.

Longer voyages meant fewer available ships.

Fewer available ships meant tighter capacity.

Tighter capacity meant stronger freight rates.

The market regained some pricing support.

And this is what makes shipping such a psychologically exhausting industry:

profits often depend on disruptions nobody actually wants.

Congestion becomes profitable.

War risk becomes profitable.

Delays become profitable.

Operationally, everyone suffers.

Financially, carriers sometimes benefit.

That contradiction has always existed in container shipping, but after 2020 it became impossible to ignore.

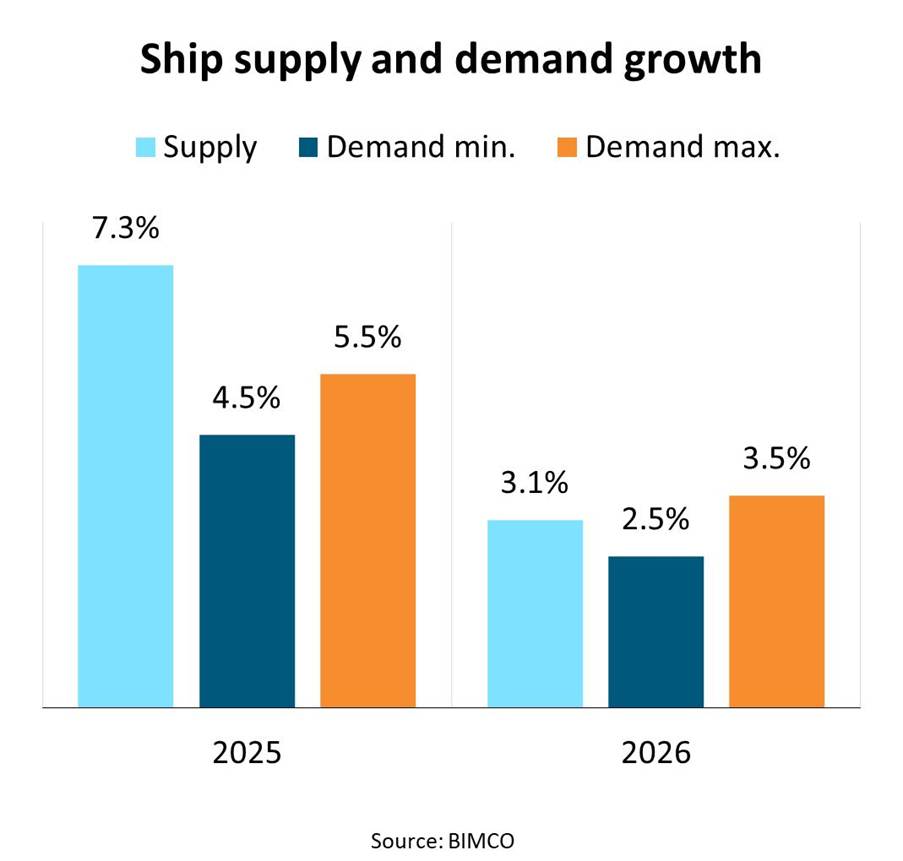

By 2025, the industry finally returned to earth

The numbers stabilized, but margins weakened again.

And honestly, this may be the most important phase of all.

Because now we are seeing what shipping looks like after the extraordinary years are over.

The easy money is gone.

Customers negotiate harder.

New vessels keep arriving.

Competition has returned.

Today, Maersk is not trying to become the biggest shipping company.

It is trying to become the hardest logistics company to replace.

That is a completely different strategy.

What most people still misunderstand about Maersk

Many outsiders still think Maersk is mainly a shipping line.

It is not anymore.

Yes, ocean freight still defines the headlines.

But the company increasingly behaves like a global supply-chain infrastructure operator.

That distinction matters.

Because the future of logistics may not belong to the carrier with the biggest fleet.

It may belong to the company controlling the most integrated network:

ports, warehouses, customs, inland transport, air freight and digital visibility.

And Maersk seems to understand that earlier than many competitors.

The real lesson from these five years

After following trade markets for years, one thing feels obvious now:

Globalization did not become weaker after the pandemic.

It became more nervous.

Companies no longer assume supply chains will always work smoothly.

Governments no longer assume shipping lanes will remain politically safe.

Importers no longer trust “just in time” inventory models the same way.

The world still trades heavily.

But now it trades with anxiety.

And that anxiety changed shipping forever.

Looking at Maersk’s journey from 2020 to 2025 feels less like reading a balance sheet and more like reading a diary of the global economy.

Every spike in profit reflects fear somewhere else.

Every collapse reflects normalization.

Every recovery reflects another disruption.

That is why I think the most interesting part of this story is not the money.

It is the realization that container shipping — once treated as a background industry — has become one of the clearest mirrors of geopolitical tension, consumer behaviour and economic uncertainty in the modern world.

Popular Posts

Explore Topics

Comments